Tip of the Week

Looking to learn more about the specifics of personal finances, budgeting, and having money conversations? Browse our recent posts to learn more about the kinds of situations we can help with.

The Dual Path: Credit Score ImprovementAlongside Debt Repayment

By Leanne | | Uncategorized

In today's financial landscape, credit scores wield significant power. Whether you're lookingto secure a mortgage, finance a vehicle, or even land a job, your credit score can be thedetermining factor. The intriguing duality of credit score improvement and responsible debtrepayment can't be overlooked. It's a symbiotic relationship that, when managedstrategically, can lead to a brighter financial future. Understanding the Connection A credit score is a numerical representation of your creditworthiness, indicating thelikelihood that you'll repay borrowed funds. It's derived from a complex algorithmconsidering factors like payment history, credit utilization, length of credit history, types ofcredit used, and recent credit inquiries. Remarkably, one of the most effective ways to boostyour credit score is by responsibly managing your debts. The Power of Debt Repayment Debt, when handled recklessly, can spell financial disaster and harm your credit score. But,when managed prudently, it can act as a springboard for credit score enhancement.Responsible debt repayment ...

5 Credit Card Frauds and How to Avoid Them

By Joe Moore | | Tip of the Week

Credit card fraud is a kind of identity theft, so you should take measures to protect your identity when you do any online credit card transaction. It’s also possible to verify the identity of anyone you deal with online. Jumio offers an online identity verification product. Click here to know more about it and how to protect yourself from identity theft. Read on for information about credit card fraud. What is fraud? If someone commits fraud, it means they did something to cheat another person. The victim often loses money, so fraud is a form of stealing. Sometimes, the victim loses something intangible, such as their power to achieve something, or even their identity. One of the most common forms of this crime is credit card fraud. What is credit card fraud? Credit card fraud is a deceptive action done specifically to deprive you of money, or your banking identity. ...

Debt Management in Times of Inflation: Strategies for Success

By Grant Chen | | Uncategorized

In times of economic uncertainty, managing debt can be one of the most effective ways to ensure financial stability and keep one's finances on track. However, rising inflation can often seem like an uphill battle. This blog post lists steps to manage one's debt effectively despite rising prices and shows how to use targeted strategies to succeed. The link between credit and debt Understanding the relationship between credit, debt, and inflation is vital to staying financially stable. Credit definition shows that credit can be a useful tool, allowing individuals to invest in purchases such as cars, but it can also lead to debt if not used responsibly. When individuals borrow money, they create debt. Inflation occurs when the purchasing power of money is reduced, which increases the cost of living and makes it difficult to pay off debt. Therefore, it is important to carefully manage the use of credit and ...

5 Benefits of Paying Off Student Loans Early

By Joe Moore | | Tip of the Week

Student loan debt is a big problem for those who incur one. According to the student loan debt statistics from the Education Data Initiative, 42.8 million Americans have a student loan debt. Student loans are a fact of life for many Americans. Paying off student debt, especially with high student loan interest rates, can sometimes be impossible. For this reason, some people choose to pay off their student loans early. But is it really the right thing to do? This article discusses the benefits of paying off student loans early and shows various ways to do so. It also lists down possible disadvantages of paying off student debt early. Knowing the benefits of prioritizing paying off your student loans early can help you make informed financial decisions. While it’s difficult to consider making advance payments when you have other financial obligations, paying off your student loans earlier than expected can ...

How To Save Money When Grocery Shopping

By Daryl | | Tip of the Week

In times of inflation, like the present times, you can always expect that the cost of your groceries each week will be a little higher than you’ve been paying. Depending on circumstances, your grocery bill could be significantly higher, and leave you wondering if something expensive accidentally fell in your shopping cart. Of course, the cost of groceries will rise all on their own, without the added momentum of inflation, so you’ll pretty much always have to keep an eye on your costs. When you first move into a new area, you may not know where to go for your grocery shopping, or you may have several choices. In that case, you can use Area Guides to direct you to the best place for your weekly grocery shopping. For some really useful tips on saving money when grocery shopping, we’ve provided the information below. Take a shopping list with you ...

How to Overcome a Fear of Dealing with Your Finances

By Joe Moore | | Tip of the Week

Photo by Elisa Ventur on Unsplash There are plenty of people who list financial stress as one of the top contributing factors to the overall stress in their lives. They feel a constant pressure to keep up with their finances even though this is not easy for them. They feel a dueling pressure to keep up with it all and a recognition that they don't know everything that they need to know about their finances to stay on top of them. Some people actively seek out CBD gummies for hair loss because they begin to lose their hair as a result of some of the stress that they are experiencing in life. They can potentially take some gummies to try to reverse their hair loss situation. In the meantime, we want to talk about some of the steps that one can take to overcome their fear of dealing with finances. ...

Navient Student Loan Settlement: Who, What, When & How?

By Holli | | Tip of the Week

The settlement reached last week with Navient is intended to resolve claims that Navient allegedly improperly steered some federal student loan borrowers into forbearance – instead of federal student loan relief programs, like Income Based Repayment, and issued high-interest private student loans to borrowers attending predatory for-profit schools where they were unlikely to succeed or be able to repay their loans. Navient consistently denies any wrongdoing. Forgiveness for Some Private Student Loan Borrowers The settlement agreement includes provisions for student loan forgiveness for certain Navient private student loans, and modest restitution for some federal student loan borrowers. Pay attention to those key words! Here’s what you need to know: If you have PRIVATE NAVIENT student loans, only certain ones issued by Navient are considered.You must have attended certain for-profit educational institutions like DeVry.The loans must have been disbursed between 2002 and 2014.You must have been delinquent for at least seven ...

Student Loans: Payment Pause Extended Through May 1, 2022

By Holli | | Tip of the Week

Hear ye! Hear ye! Okay, now that I hopefully have your attention…the “rumors” are correct. If you have federal student loans, your payments do not (have to) begin again until May 1, 2022. If you were unaware, they were due to begin end of January 2022. Why the “have to”? If you noticed, I said do not (have to) begin again. Because if you CAN afford to pay now, paying your student loans now while NOT accruing interest is a VERY WISE FINANCIAL DECISION. You can make a bigger dent in your repayment of loans if you can pay while no interest is accruing. It’s math. This pause includes (continues) the following relief measures for eligible loans: A suspension of loan paymentsA 0% interest rateStopped collections on defaulted loans Scam alert: Do not accept unexpected offers of financial aid or help (such as a “pandemic grant” or “Biden loan forgiveness”) ...

BNPL?? What the Heck Is It? And What the Heck is It NOT?

By Holli | | Tip of the Week

Recently, I had a client with a multitude of small payments due that I was wondering what is going on here? They were adding up SO fast that the client had simply lost track and needed some help. Welcome to BNPL. Buy now, pay later (BNPL) is a payment plan that lets you break up your total purchase at checkout into a series of smaller installments. These plans aren’t new…but recently have been catapulted into the mainstream with Amazon, Walmart, and Target now offering them. But with the promises of convenience, zero interest and minimal fees…you have to wonder…what’s the catch? Guess what BNPL accounts are NOT? Helpful to your credit. BNPL providers don’t report on-time payments to the major credit bureaus, so unlike credit cards or loans, you can’t build credit with this type of financing. BUT here’s the catch…some providers DO report missed payments which ultimately hurt your ...

How Not to Get Wrapped Up in Holiday Overspending

By Holli | | Tip of the Week

Give yourself the gift of a “financial stress-free” holiday this year! You deserve it. It’s been a hard-enough year. It IS possible to celebrate without spending all of your cash or maxing out your credit cards. Stay on budget…and don’t get wrapped up in holiday spending!! (See what I did there?) Set Holiday Spending Limits Limit yourself and give your mind a break (and your credit card) by limiting what you buy to ONLY what can safely come out of your bank account. (Or your cash amount.) How much can you actually afford to spend? Holiday budgeting is a way to set limits on your purchases and still enjoy the season. Or maybe because of it! The money you can reasonably spend on gifts is money that isn’t going to bills. If you want a little more to spend, it doesn’t have to be solely from what’s left after bills ...

YOU & YOUR CREDIT REPORT: Understand It!

By Holli | | Tip of the Week

It’s easier to review your credit report successfully when you know and understand all the parts, what they mean, and how they affect your credit situation. AND....GO... Personal Information Credit reporting agencies use your personal information to confirm you are the person who opened the accounts listed on your report. Check this section carefully to make sure your information is correct and current. The wrong information could mean that you are being charged for another person’s debt! Public Records Bankruptcies (sometimes foreclosures) are the only public records that appear on a credit report. They appear as long as 10 years. Negative information may lead to a higher interest rate or being turned down for credit. Account Information In this section, your credit accounts are displayed one by one. Lenders typically update the information monthly. The information usually includes: payment history, if an account is current or past due, balance, and ...

Buyer Beware! Looking for Alternatives for Your Holiday Shopping?

By Holli | | Tip of the Week

You’ve probably been hearing all about this: THIS holiday season, it might be harder to find the gifts you’re looking for. Many of us are looking for alternatives, like buying locally – or maybe from online marketplaces, social media sites, online ads, etc. If that’s you heading online, here are some tips you can do to avoid a scam or bad experience: CHECK THE RULES. Check the rules about refunds and returns, and what happens if there’s a problem. Does the site have processes to help you get the refund if you don’t get exactly what was advertised or if you never get the item? PAY IT SAFE. Make sure they let you pay with a safe payment method. For example, credit cards have legal protections, or a secure online payment system can protect you in case there’s a problem. IF someone tells you to pay with a wire transfer, ...

Common Debt Payoff Mistakes…Just Don’t Do It! (Pt 2)

By Holli | | Tip of the Week

You didn't think I would forget the second part of the most common debt payoff mistakes, did you? Read on... 7. No Plan To successfully get out of debt, you need a plan. Very simple. Throwing money at various debts is okay. However, with a plan, success happens FASTER. Knowing when a debt will be paid off with a plan is a HUGE motivation. You can SEE your progress. 8. Lack of Motivation Speaking of motivation, it is HUGE when paying off debt. This common debt payoff mistake will make or break your success. You need to keep your motivation going. One of the best ways is to plan milestone celebrations. They don’t have to be huge or costly. Track your progress visually with a debt tracker. 9. Wicked Debt Cycle The continuous debt cycle is harsh. This common debt payoff mistake is why so many try to pay off ...

Common Debt Payoff Mistakes…Just Don’t Do It! (Pt 1)

By Holli | | Tip of the Week

I get it. I get it. We are regularly writing these articles to review how to become debt free and suggest relatively the same steps over and over again. But maybe, just maybe, in the midst of those steps, you are also making a few mistakes when it comes to your debt payoff plan! Read on... No Emergency Fund Probably the number one mistake when attempting to pay off debt is no emergency fund. Do not be afraid! I'm not saying the 6 months of living expenses saved up...but what about something to start. Not setting aside ANY money for the "unexpecteds" is the mistake. Start with a goal of $1000 or $500. Something. When you are reorganizing and trying to get ahead with your finances, you must start on a solid foundation. That means an Emergency Fund. In order to get ahead, you must be prepared for the unexpected. ...

Don’t Be Surprised! 5 Things That Might Stop You from Getting a Home Loan

By Holli | | Tip of the Week

Before you even fill out the application for a home loan, make sure you’re prepared. Here are 5 things that might stop you from getting a mortgage. Your Credit Score Isn’t What You Think It is Did you know that you have more than one credit score?? Fewer than 10 percent of Americans know this. Don’t rely on free credit scoring websites. Go to one of the three FICO-approved credit bureaus – Equifax, Experian, and TransUnion. For a free FICO score, check with your bank or credit card issuers. Recent Changes to Your Job or Income While it is possible to get a home loan after a recent job change, it can be tricky. IF your income structure changes significantly like moving from a salary to commission, it can be trickier. A lender calculates your average salary over the past 24 months when evaluating your application. Your change in pay ...

Secured Debt v. Unsecured Debt: Smart Debt Repayment Strategy

By Holli | | Tip of the Week

Secured Debt is… Debt is secured when the creditor takes a “security interest” in collateral. Sounds confusing but the concept is simple. For some types of debt, creditors want to know what they can get their money back without too much trouble if you don’t pay them. Taking a security interest accomplishes this. For personal debts, the language creating the interest if included in the contract that the borrower signs when purchasing the collateral. That security interest gives the creditor rights to the collateral. Collateral is simply property that you pledge to give the creditor if you fail to pay the money you owe them. Collateral on secured debt for personal use is the very property that you purchased with the loan you were given. Two simple examples: mortgages and auto loans. The collateral is the house or vehicle. In a car loan, the creditor who is making the auto ...

Student Loan Payments to Restart: Here’s How to Get Help

By Holli | | Tip of the Week

Repayment starts as of October 1 for 4.29 million student loan borrowers with federal debt. It’s been 18 months without a payment. That ends in October - ready or not. The interest-free federal student loan payment pause, known as forbearance, was extended three times after it initially went into effect in March 2020. But with payments set to resume in a few months, servicers – the companies that manage student loan payments – are already fielding thousands of calls a day from borrowers seeking student loan help. Time is running out for both servicers and loan borrowers to prepare for repayment. Education Secretary Miguel Cardona has indicated that it is not “out of the question” to extend the loan forbearance, borrowers should be prepared for bills to come due sometime in October. (You should be notified 21 days prior to your exact billing date.) What to do?? TALK WITH YOUR ...

Today’s the Day! Child Tax Credit 2021

By Holli | | Tip of the Week

The federal Child Tax Credit (CTC) is kicking off its first monthly cash payments on July 15 to eligible families with children ages 17 or younger. Almost 9 of 10 payments were sent via direct deposit according to the IRS and Treasury. The enhanced Child Tax Credit is an expansion that boosts the credit from $2,000 to $3,600 for children ages 6 to 17. It also makes the CTC “refundable” which means people can get it even if they don’t owe federal income tax. Not everyone will qualify. Single taxpayers must earn less than $75,000 and joint filers must earn less than $150,000, with payments reduced by $50 for every $1,000 of income above those limits. The enhanced payments phase out for single taxpayers earning $95,000 and joint filers earning $170,000 – but most households earning above those limits will still qualify for the regular $2,000 per-child CTC. These payments ...

When is the Best Time to Buy Your First Home?

By Holli | | Tip of the Week

Buying your first home is both thrilling and challenging, and not for the faint of heart. Before you even get into the housing market, you will spend quite a bit of time thinking about your goals and preparing your finances. One the most difficult decisions can be figuring out when you are ready to enter the market and to start placing offers on homes! This process looks different for everyone. Bottom line: There is not a single right time to buy a house. Here are some tips for how you can determine the ideal time to buy your first home. Three Major Considerations Because this is such a major decision, you need to think about it through multiple lenses. If you let emotion take over, you will be much more likely to make a mistake. Here are the three different ways you should think about the decision to enter the ...

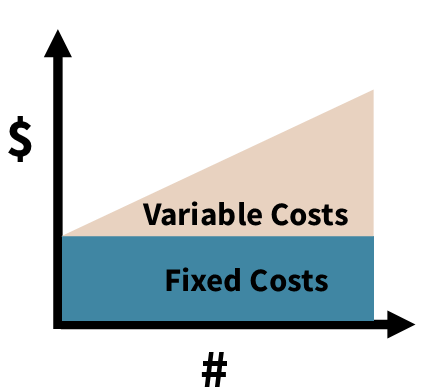

10 Ways to Lower Your Life’s Fixed Costs

By Holli | | Tip of the Week

Household budgets are comprised of two types of expense: fixed and variable. A fixed cost is an expense that does not change from one month to another. These are expenses that have to be paid. Think mortgage payment, rent, insurance, etc. But the exact money spent on clothing or ice cream varies wildly from one month to another. A variable cost. But you CAN make changes to fixed costs. Then more money in the budget and more money in the bank.. Here are 10 tips that may reduce your fixed costs.? Buy/Rent a Smaller Home. Housing costs take up the largest percentage of a person’s income in most cases. Living in a smaller home offers opportunity to cut these fixed costs. Your largest expense offers the greatest opportunity.Avoid Car Payments. Best car advice: “Buy the most reliable car that you can purchase with cash, and then begin saving for your ...

ATTENTION WI PARENTS: Pandemic EBT Benefits

By Holli | | Tip of the Week

Nearly half a million Wisconsin children are eligible for Pandemic EBT benefits, but many parents may not know it. Starting in March 2021, this program will provide grocery store benefits to parents to replace the value of missed school meals. Pandemic EBT (or P-EBT) is a federal nutrition program that the USDA has recently approved in Wisconsin for families with school-aged children. Benefits are based on the 2020-2021 school year and will be available starting March 25. What is Pandemic EBT? Pandemic EBT (P-EBT) is a program at provides grocery benefits to parents to replace the value of missed school meals. That means you can receive money for groceries to help feed your children – families in WI could receive up to $1,248 per child! Children who did virtual learning (learned at home or on a home computer) for any portion of the 2020-21 school year may be eligible to ...

Simplify Your Finances, Improve Your Quality of Life

By Holli | | Tip of the Week

There are many ways that simplifying improves your quality of life. But let’s focus on FINANCES. One encouraging effect of simplifying is that it also saves you money. Decluttering and simplifying makes you more thoughtful of what you purchase going forward. You see what you have wasted money on and reign in your purchases, which then helps keep clutter out and money IN! Do these simple things and see how much money you can save! WAIT TO PURCHASE Don’t get caught up in the advertising hype. It’s easy to do. Marketers are professionals and they know what they are doing. Before you know it, you’re clicking away and ordering something you’re convinced you HAVE to have. They tell you that you deserve it or that it will improve your life in some way. Very few things live up to what they promise. More often, they turn into buyer’s remorse and ...

The 5 Worst Money Mistakes You May Be Making

By Holli | | Tip of the Week

We ALL make mistakes. That’s a given. And we all know about learning from our mistakes. You’re not alone if you’ve made a few financial mistakes. While money mistakes are arguably subjective, there are a handful of missteps that experts agree you can easily avoid. Here are 5 common money mistakes and steps you can take to avoid them: 1. NOT HAVING AN EMERGENCY FUND If 2020 taught us anything about our finances, it’s the importance of having an emergency fund to tap into when unexpected events arise such as job loss or unplanned medical bills. When you have no extra cash set aside, then you’re forced to use expensive ways to finance your life. This can (and usually does) include racking up high-interest credit card debt, taking out a cash advance, or relying on (the dreaded) payday loans. These financing options will also be tied to what kind of ...

Spot a Credit Repair Scam

By Holli | | Tip of the Week

January is the month of “new beginnings”, “fresh starts”, “do-overs”. And finances usually top the list. Don’t be fooled by credit repair scams. Good credit is important for many reasons. It makes it easier to get a credit card or loan with favorable terms. Bad credit can make it difficult to rent an apartment, find a new job, or get a cellphone contract. It’s easy to see why someone with bad credit, who is desperate for help, will fork over hundreds of dollars (sometimes thousands) to a company that guarantees to solve their credit problems. It's THIS simple. Any company that promises it can hide or remove your bad credit history for a fee is scamming you. If you believe the ads—and you should not—these “credit repair” companies can quickly and dramatically boost your credit scores by removing all negative items (such as late payments and bankruptcies). “The reality is ...

STIMULUS CHECK: ROUND 2

By Holli | | Tip of the Week

Have you checked your bank account? Yours may be one of the bank accounts that already has the $600 stimulus check deposited! This second round of stimulus direct payments started December 29, 2020. The checks will continue to hit bank accounts (or mailboxes via paper check or debit card) through the first half of January 2021. HOW DO YOU FIND OUT IF YOU QUALIFY? Qualifications is similar to the first round of stimulus payments in March 2020. Individuals earning up to $75,000 a year and couples earning up to $150,000 a year are eligible for the full amount. Parents can receive an additional $600 for each dependent child under 17 years old. WHAT IF YOU DON’T RECEIVE A SECOND CHECK? Most people will receive their second stimulus check by direct deposit with the bank account that the IRS has on file. Payments are automatic for anyone who filed a 2019 ...

2021: A YEAR OF POSITIVE GROWTH

By Holli | | Tip of the Week

A new year, a new you. We've all heard that, right? But what if you like the old you and maybe just need a little boost? Make 2021 your saving-savvy, year of positive growth. Start with one or two tips below. But START! BE SCARED OF CONSUMER DEBT... But not necessarily of credit cards. Keep reading. There are HUGE benefits to using credit cards RESPONSIBLY. You need to build a credit history. You need to build a clean, excellent credit history. Start with a secured card. This is where you put down a deposit which becomes your credit line. You treat the account like a regular account and make payments ON TIME. Use the card responsibly here and there. Pay off the entire balance immediately when you do use it. In no time at all, you will have built a credit history and did so in a safe way! START ...

FINANCIAL FREEDOM 2021!!

By Holli | | Tip of the Week

Get ready! 2021 is literally around the corner! And just like starting fresh in the new year is a great goal for weight loss, exercise and all the other common new year's resolutions...it's the perfect time to think FINANCIAL FREEDOM in 2021!! This past year has been a rollercoaster. No doubt about it. Time to take control and feel the power you can obtain over your finances. DEBT FREE does not equal wealth. OF COURSE, becoming debt free is one of the MOST freeing accomplishments. Focus on it; however, know that it does not equal wealth. While increasing your monthly cash flow and reducing debt is VITAL to move on in your financial freedom, there are options in HOW to do so while also preparing to build wealth. It's all about the numbers. Remember your math teacher, telling you how important math would be in your life??? Create a moderate ...

Holiday Shopping Tips 2020

By Holli | | Tip of the Week

FTC (Federal Trade Commission) reminds shoppers to look out for scams and do your research to save money. Holiday shopping has taken on a new shape this year due to the COVID-19 pandemic. Likely you'll be going online to look for those perfect gifts. With endless sales going on, it's important to keep some online shopping tips in mind. Holiday Shopping Tips Most importantly, make sure your computer is outfitted with up-to-date antivirus software. The FTC has published a comprehensive list of things consumers can do to make sure their cybersecurity is up to snuff. While you are doing your actual shopping, there are steps to ensure you're getting the best deal and keeping yourself safe. * Take time to compare products. If you're looking for a specific item, take the time to shop around. Doing so can allow you to save money that can be used for other gifts ...

STEP BY STEP: HOW TO BUILD SMART FINANCES

By Holli | | Tip of the Week

Holli Lewandowski; Certified Credit Counselor and Credit Educator Recently I spoke with a group of high school students who had been discussing personal finances in a life skills class. They had many great questions and so it had me thinking…what would I have wanted to know as a young teen that I now know regarding building smart finances?? Save/Spend/Share From the youngest of ages, children can be “primed” to see their finances as having power. The power to share and make a difference. The power of compound interest. The power of saving up for that special something. Smart money management is a muscle. Keep using the skill and it will get stronger. Teach your children (or start again with yourself…it’s never too late!) to divide your money into the above categories or something similar. Save: that’s they easy one…in a piggy bank or a real bank account. Spend: this amount ...

UPDATE: What Renters Must Know About Eviction Moratoriums

By Holli | | Tip of the Week

There have been new changes to the legal and economic landscape for renters. The CDC published an order that protects qualifying renters who have been impacted by COVID-19 and submit a proper affidavit. However, that order expires at the end of the year. A few other federal protections may help some renters, and individual states have also published their own orders. Here is a closer look at the protections currently in place for renters impacted by COVID-19 along with some ideas for how to maintain your rent payments moving forward. The CDC published an order forbidding evictions of “covered persons.” This order is effective through December 21, 2020. In some ways, this order is more expansive than the previous moratorium under the CARES Act, because it covers more people. The CDC order actually applies to every rental unit. Tenants must certify that they are qualified as a “covered person.” Tenants ...

7 Biggest Money Wasters and How to Avoid Them

By Holli | | Tip of the Week

The pandemic has caused us all to take a second look at our spending habits. And it’s more important than ever to recognize where you can cut back and save. An easy place to start is looking at your spending habits and recognizing when it is that you spend when you don’t need to spend. This money could be added to your emergency fund or saved for holiday shopping, which often seems to come as a surprise each year. Now is a good opportunity to zero in on where your money goes and break the habit of spending on things you don’t need. Below are seven (and unexpected) ways people waste money and how to avoid these costly mistakes. Stop paying for insurance that you don’t need This one goes overlooked. Many times, people believe that the more insurance, the better. Certain forms of insurance are just not necessary for ...

7 Key Pieces of Financial Advice to Unlock Your Life

By Holli | | Tip of the Week

The lightbulb moment. The "ah-ha" moment. When algebra finally makes sense. Those are the KEYS that change your life. The following 6 are those moments financially: 1. People who overspend their income do so in one of three ways: 1) Too much house, 2) Too much car, 3) Too much entertainment. Of course there are outstanding circumstances (medical emergencies, tragedy, job layoff, etc.) But generally speaking, if you have a hard time living within your income, check your spending on your home, your car, or your entertainment (dining, tickets, trips, shopping). Keep each category modest a.k.a. "live within your means". You can't have a steak dinner on a hot dog budget. But with the correct financial outlook and planning, you can have that future lobster dinner without debt or anxiety. 2. Begin your marriage/partnership living on just one income. Imagine this: Work hard to live on just one of the ...

Protect Yourself from Cyber Attacks!

By Holli | | Tip of the Week

How to keep your information safe: Make sure you know who you are communicating with. Fraudsters pose as legitimate organizations like banks, the IRS, etc. There are some basic things to remember. Text message: Your bank will never ask you to sign in or give personal information via text message.Email: Watch out for emails that tell you to click on a link or provide personal information.Phone Calls: If you didn’t expect a call from the bank, it could be a scam. Don’t provide any personal information, just hang up, and call the bank yourself at the number in your banking information. Be aware of COVID-related scams. Criminals are taking advantage of the pandemic. Here are some of the top 5 scams to look out for: Stimulus Scams: Be alert of scammers asking for an upfront payment, bank account, or social security information in order to receive your stimulus check. The ...

WARNING SIGNS: Are you stuck in debt?? (Part 2)

By Holli | | Tip of the Week

Are you stuck in debt? These are the continuation of warning signs. OVERWHELMED BY STUDENT LOANS Student loan debt has reached $1.5 trillion! And more than 9% are at least 90 days late. Solution: Speak to a school loan counselor to identify options like income-based repayment or consolidation. Avoid it in the first place: grants, scholarships. Weigh the cost v. your earning potential as a guide to loan totals. YOU ALLOW FOMO TO DICTATE YOUR SPENDING One of the biggest causes for overspending and debt is FOMO. It's a real thing. Solution: Use cash instead of credit to really think about your spending decisions. It's a form of mental accounting. YOU HAVE YOUR FINANCIAL PRIORITIES MIXED UP One of the most common mistakes is to think that when it comes to credit card debt, that you need to save and invest at the same time. Any money that you are ...

WARNING SIGNS: Are you stuck in debt?? (Part 1)

By Holli | | Tip of the Week

80% of Americans are in debt. $13.95 trillion (yes, with a "t".) This is the total amount of debt from the most recent report on household credit and debt. (Federal Reserves of NY) Read those again. Are you stuck in debt? There are warning signs. YOU BELIEVE DEBT IS PART OF LIFE Nope. Debt is the result of wanting or needing something that you don't have the finances to buy at the moment. Simply put. Solution: Don't WANT debt so badly! Keep close tabs on your spending to see how much you're relying on debt to maintain your lifestyle. YOU USE CREDIT TO COVER EMERGENCIES When you don't have cash reserves to cover unexpected expenses, you might have to rely on your credit cards. Then you end up paying more than the original emergency if you don't pay off the balance before interest charges begin. Solution: You can avoid this ...

The 16 Day Guide: Get Started on Becoming Debt-Free

By Holli | | Tip of the Week

You can do it! It will change your life. **This is NOT a guide to becoming debt-free in 21 days but instead 21 days of motivation, inspiration, and action to FINALLY get started!** This is a guide to change the way you think about money. Day 1: Plan with your partner (or self) a day to review finances, health, and other things that are meaningful to you. Set the date. Write it down, Commit to it. Choose a time when you can have an hour or two with no kids or distractions. Have a conversation. Daydream a bit…” I think it would be awesome to…” Ask questions like why now or why not now? Set up another time to check in. Day 2: See your money on paper. WRITE it all down. What’s going in. What’s going out. What you own. What you owe. Day 3: Let go of the ...

“NO” IS NOT A NAUGHTY WORD: GOOD FINANCIAL HABITS

By Holli | | Tip of the Week

Most of us make poor financial decisions: a trip we can’t really afford or repeatedly eating lunch out when our budget says “brown bag it”! Making small changes over time can have a major effect on your finances. Your finances are generally a series of little choices that add up over time – buying one latte that you really can’t afford won’t necessarily ruin your finances. But those small bad choices add up to debt, regret, and major issues in the long run. Turning things around doesn’t have to be hard or painful! Make just a few small changes, and you’ll be on track for a meaningful improvement to your finances and you can start at any time! Why not start NOW? ** MAKE A BUDGET You can’t stick to a guide of a budget if you don’t have one. It’s very important to fully understand how much money is ...

REBUILD YOUR EMERGENCY FUND: 5 TIPS

By Holli | | Tip of the Week

These are tough times. No doubt about it. So what if you've used up your emergency fund? Rebuilding happens slowly. Just like the first time. But there are plenty of things you can do to help you get back to where you were. It takes hard work, but it's worth it for the security you'll get in return. LAY OUT A NEW BUDGET During any rough patch, laying out a new budget to make your money stretch is a great step. While things are probably still tight, a new budget is in order yet again. Make saving a part of your budget. You've heard it before...PAY YOURSELF FIRST. Consider automating payments like a regular bill to keep the savings constant. Start small. Once you reach your goals, establish a new spending plan. 2. FIND A SIDE HUSTLE Maybe your income still isn't what it used to be? Consider adding another ...

PAPER or PLASTIC?

By Holli | | Tip of the Week

As we move closer and closer to a cashless society, consumers can use credit cards to pay for nearly everything, everywhere these days. BUT…that doesn’t mean you should. Outstanding card debt has now hit its highest point ever, surpassing the $1 trillion mark in 2017 (per the Federal Reserve). Yes, that’s with a “T”. No wonder 86% of Americans who have or had credit card debt said they regret it, according to a recent report by NerdWallet. NEVER put these 5 expenses on credit and why! TAXES It can be tempting to put an unexpected tax bill from Uncle Sam on Visa or Mastercard. You feel like “I’ll get it over with and worry about it later.” NOT SO FAST. The Internal Revenue Service will charge a processing fee of up to 2 percent AND if you use a third-party filing software, you’ll pay even more. Why pay interest charges ...

President’s Executive Actions & Your Finances: Student Loans, Unemployment, and Housing

By Holli | | Tip of the Week

What do these Executive Actions mean for YOU? Evictions: (No Federal Moratorium for Now) The CARES Act had previously created a moratorium on evictions for federally subsidized housing and properties with federally-backed mortgages. Those protections expired on July 25. (JUST IN: Moratorium extended through December 31, 2020!!) **You can view the press release at https://www.hud.gov/press. USE AVAILABLE RESOURCES Remember, first and foremost, you are NOT alone. Many people are working tirelessly on this issue. If you need help, consider reaching out to your local housing resources, including legal aid or other tenants’ rights groups. NFCC-certified agencies (like this one) can also help with rental counseling or budget and credit counseling, which may help you restructure your personal budget and debt obligations in order to make your rent payments. Make sure you stay informed about your rights, follow any developments in a new stimulus bill, and remain in close communication with ...

SWEET 16 MONEY SAVING TIPS …JUST BECAUSE!

By Holli | | Tip of the Week

Don’t buy bottled water. Seems cheap, but it gets expensive fast. Settle for a filter and you can use tap water! Bonus: Better for the environment too. Make your own coffee. Seems obvious. Use a coffee maker or even a French press instead. Even if you add a flavored creamer…still much less painful on the budget. Throw almost-spoiled veggies in the freezer. Toss those nearly spoiled veggies in the FREEZER instead of in the trash. Use for smoothies!! Cuts your waste down too. Break out the slow cooker. Cooking in bulk really helps cut down the costs associated with more individual-size meals. Eat your leftovers. Obviously. Wash with cold water. Unless you have serious stains or odors you’re trying to remove, most clothes can wash cold without an issue. And many times, for the better! Lower the temp on your water heater. Check your water heater. You generally don’t need ...

NEW WHEELS? Don’t get fooled!

By Holli | | Tip of the Week

It’s easy to spend more then you planned when buying a car. But spending too much on car creates unnecessary financial stress. Don’t get fooled…there are a few steps you can take to stay in your financial lane when buying a car. Set a budget! Just like you do when shopping for a home, you need to know what you can afford. Prepare a monthly budget to determine how much you can comfortably afford for a car. Deduct monthly expenses, including your allotted amount for savings, from your monthly take-home pay. You can use the remaining amount for your car payment, insurance and car expenses. Do your research. Research the car you want to buy BEFORE you go to a dealership. Check out performance reviews, car values, and more. The more familiar you are with the car that you are interested in, the less likely you’ll be fooled into paying ...

YOU CAN DO IT! Ways to Save During Quarantine

By Holli | | Tip of the Week

I know! I know! You've tried it. You've heard them all. BUT have you?? There are ways to save in this unique time of quarantine. Read on... SET UP A BUDGET Your budget is your financial lifeline. List every income source you have: day job, benefits, part time, and odd jobs. Detail all your expenses, like you home payment, car loan, insurance, utility payments and anything that is mandatory every month to pay. Include gas and groceries even though they fluctuate. Create line item budgets for each category. Give a realistic estimate and check back every couple of weeks to check your status. Make adjustments as necessary. REMEMBER: Budgets are a growing, living document. It is a tool. Make sure you aren't overspending and all of you money is going where it needs to go. GET A BUDGETING APP You can use pen and paper or a spreadsheet, but you ...

RENT: What happens after evictions protections end?

By Holli | | Tip of the Week

If you live in a property covered by the CARES Act, the soonest landlords can ask you to leave is July 25, and the soonest they can file an eviction to force you to leave is August 24. THIS PART IS ESSENTIAL: The protections under the CARES Act only apply to properties that receive federal funds or are financed under a federal program like Fannie Mae or Freddie Mac. If you live in a multifamily property with five or more units, there’s a tool by the National Low Income Housing Coalition that’s designed to tell you if the property where you live is covered under the CARES Act. Just enter you zip code and scroll through the list of properties looking for yours. There are other online tools that can help connect you to other resources. 211.org connects those in need of help with essential community services. Recently it has ...

10 Warning Signs of Too Much Debt

By Holli | | Tip of the Week

You spend more than 20 percent of your monthly take-home (net) income on consumer debt. (Credit cards, loans, etc.) You don't know how much money you actually owe. You miss payments or pay them late. You have been refused credit. You have overdrawn your checking account more than three times in the past year. You borrow to pay off other debts. You only make the minimum payment on bills. Debt collectors are calling. You borrow from retirement accounts or use credit cards to pay monthly bills. You have to take an extra job just to pay your bills. Do YOU have any of these signs? Your credit counselors can help! Let's talk about it...

Savings. Do it now. It’s never too early…or too late.

By Holli | | Tip of the Week

No matter your stage of life, it's important to have savings. Special purchase? Save. College education? Save. First home? Save. Retirement? Save. Emergency fund? SAVE. CREATE A BUDGET. You must evaluate how much money you take in and how much money you spend to take control of your financial life. List your income from all sources. List your "fixed" expenses - the ones that are the same each month. Think rent, car payments, etc. List your expenses that vary - entertainment, recreation, clothing, etc. Write down ALL your expenses (even if seem insignificant) to help you track your spending patterns, identify necessary expenses, and prioritize the rest. PAY YOURSELF FIRST. This means automatically making a savings contribution or investment with your income before it even reaches your wallet. Consider a payroll savings plan where a certain amount goes directly into your savings account each payday. (One of the easiest ways ...

Stop the Cycle of Debt. Seriously.

By Holli | | Tip of the Week

SO you've paid off your debts. You're FINALLY free! Now what? The WORST thing you could do it successfully pay down your card balances, only to find yourself in debt again months or years later. Change the way you handle your finances and they way you think about money in order to keep yourself out of trouble. **If you haven't set up a budget for yourself yet, this is a MUST DO step. It will help you keep track of your spending each month so you know where every dollar is going. By using a budget, you will drastically reduce your chances of falling back into debt. Paper & pen, ledger style, spreadsheet, or even great apps on your phone...there are all kinds of budget options. USE CASH ONLY FOR NON-ESSENTIALS Cut up those cards to avoid further temptation. Consumers spend more with a credit card than with a debit ...

ID theft can happen to anyone

By Leanne | | Tip of the Week

An acquaintance recently shared this story with me: Ken, I have read your articles on identity theft in the past and have taken many of the precautions you have suggested. I take a great deal of pride in knowing about all of the precautions, and said "it could never happen to me, I am too careful." I would like to tell your readers to take identity theft seriously. Recently, I was shopping for a television, Internet, phone and cellular service that would meet my needs and hopefully save some money. One of the providers offered me a special promotional package that gave me more for less and saved me approximately $30 a month. I think you would agree this deal was too good to pass up. Again, being a smart consumer, I put the service on my credit card so I could get the reward points from the credit card ...

Some deals are worth waffling on

By Leanne | | Tip of the Week

August 1, 2010 Have you ever noticed how easy it is to rationalize your spending habits? There is nothing like something free, reduced, on sale or marked with a clearance sign to get the old shopping adrenalin going. I was walking through a store the other day, and as a good consumer, and following my own advice, I was checking out the sale and clearance aisles in the store. As I browsed the shelves of bargains, I found one of those things I couldn't live without, a waffle maker. Up to that point in my life owning a waffle maker had never crossed my mind, and I would have never considered purchasing one at full price. But this hidden jewel was too good to pass up. It was the display model, without the box or manual for only $9. I was going to save 80 percent; that's right 80 percent. ...

Saving is tough, but it can be done

By Leanne | | Tip of the Week

Dear Ken: You keep talking about saving for emergencies. But my wife and I are having a hard time making ends meet. We know we should save, but it is almost impossible. Do you have any special tricks that might work? A: Saving in tough times, or for that matter, saving anytime is tough. There are two basic rules of saving — spend less than you earn and have a reason to save. Part of the problem is the perception that we have to make a huge sacrifice to save. When times are tough, the temptation is to cut back on saving and focus on surviving. However, when people start thinking about ways to save and start cutting back a little in several areas, they find they can save more. Here are a couple of thoughts for you to ponder. First, get the entire family involved in the process.Let everyone ...

Having the 'money talk' with spouse

By Leanne | | Tip of the Week

June is just around the corner, wedding bells are i n the air and I can "feel the love." If there was one thing I could share with newlyweds, it would be that sometime between "Yes, I will marry you," and "I do," you need to have the "money talk." Couples don't fight over love. They fight over money. They fight because they can't balance the checkbook or one of them makes a major purchase without talking to the other person. Whether the issues are big or small, money will affect your marriage. Here are the four things you need to include in the money discussion that will give you some insight into how money will flow through your marriage. • Assets and liabilities. Take a look at what you both have and what you both owe. Assets are bank accounts, investments, cars, houses, and all of the other "stuff." ...

Foreclosure purchase not always a deal

By Leanne | | Tip of the Week

Dear Ken: I read your column on buying a home. What do you think about buying a foreclosure home? Answer: There's a myth that all foreclosures are deals because they can be purchased for pennies on the dollar. But not all foreclosures are deals and steals. Foreclosures often are purchased below market value, but the reduction in purchase price may only be 10- to 15-percent of the market value of the home. That savings should be considered against some of the risks. Basically, there are three ways to buy a foreclosure property: >> 1) pre-foreclosure sales; >> 2) foreclosure auctions or sheriff's sales; and >> 3) from the lender after the foreclosure sale. In a pre-foreclosure sale, you buy the property from the owner before it goes to auction or sheriff's sale. Sometimes this may be at a discounted price or may be a short sale (a sale for less ...

Ways to alleviate debt stress

By Leanne | | Tip of the Week

Dear Ken: We are in a financial crisis. My husband is a carpenter and in the last year and a half work has been hard to come by. I am currently working at a factory job and have had my hours reduced. We are having a hard time making all of the payments on our credit cards, medical bills and mortgage. We have used up our retirement savings and have had to use credit cards to survive. The stress is getting to us, and we don't know where to turn. Where do we go to get help? A: I guess our agency is still one of the best-kept secrets in the county. What you need to do is contact our agency for a financial assessment. The process is quite simple and non-intimidating. You call the office, we send you a simple worksheet and when it is completed you call for ...

How prepared are you for the unexpected?

By Leanne | | Tip of the Week

Are you ready? Not too long ago, I was with my mother in the hospital. We were there because my father had some serious health concerns and we were considering the options facing the family. I was amazed at how well my mother and father had planned in case something would happen to either one or both of them. I know that we are all going to die sometime. Our financial planning is important, and the details are worth spending a little time and consideration on. If something such as death or serious illness hits, are we ready, or are our spouses or survivors ready to take care of the financial matters? All too often I have seen a spouse or survivor in a total quandary in these circumstances. Here are a few things you might not have thought of or considered in getting it together. First, do you know ...

Build a 'bridge' to a happier retirement

By Leanne | | Tip of the Week

I was talking to a friend the other day and he made the observation that a lot of people our age are starting to look old. I had to agree with him and shared that I had noticed that he and I were aging much better than a lot of our other friends. He was considering retirement, but thinks he would still like to keep working. I shared that I had read an article about staying young. The article pointed out that if you want to stay healthy after retirement, you need to keep working. That is exciting to me — a not so successful "recovering workaholic." The research and findings were from a study done at the University of Maryland. The researchers found that people who transition from full-time employment to full-time retirement with part-time work, experienced fewer major diseases and functioned better day-to-day then those who totally quit ...

Getting out of debt takes family effort

By Leanne | | Tip of the Week

Dear Ken: My wife and I would like to get out of debt. We are stressing out about our money situation. We are sick of fighting over money and really would like to work our way out of debt. What do we have to do? A: I am glad to hear that you have accepted the fact that it needs to be a family effort. Debt and spending habits can cause a lot of stress and strain on marital and family relationships. The question is: Are you are ready and willing to change your lifestyle and spending habits to get out of debt? If you are, you are going to have to change some basic attitudes and habits. The entire family must be involved, not just you and your wife. Relief is called " positive cash flow." All you need to do is spend less than you earn. So if ...

Credit card bailout program does not exist

By Leanne | | Tip of the Week

Dear Ken: I saw an ad on TV last night and also on the Internet that there is a government bailout program for people with credit card debt of more than $10,000. It would allow us to pay off our debts for 60 percent of what we owe. What do you know about this program? A: There is no bailout for consumers with credit card debt of any amount. What you saw is a scam known as debt settlement and it will ruin your credit score. Last week, I worked with two different individuals who paid thousands of dollars to one of these groups. The groups provided absolutely no service and the individuals are ending up in the legal system with judgments being filed against them. The "credit card bailout" ads are very careful not to say they are government programs. The ads only imply there is help. In many ...

Scams strike good people

By Leanne | | Tip of the Week

You have heard the saying, "Bad things happen to good people." Last week I heard of two people who were scammed by being good people. It happened in Madison, just outside a credit union. On two different occasions, a man approached a credit union member, asking each of them for help to cash a personal check. He explained that he and his family were stranded in Madison on their way back to New Jersey, and he needed to cash a check for gas and food so they could get back home. He said that because he didn't have an account at the credit union or an ATM card, the credit union wouldn't cash the check for him. So the man asked both people if he could make a personal check payable to them. Both people could cash the checks and keep $10 for their trouble, give him the rest of ...

Use your tax refund wisely

By Leanne | | Tip of the Week

Dear Ken: I just finished my federal and state taxes, and I am getting a nice tax refund of more than $3,500. What would you suggest I do with it? A: First, take a deep breath. If you are like most people, you already have plans for that refund, and you should know that by asking me there probably won't be anything fun you will get for your money. With that said, I would suggest looking at your personal financial situation and what options you have available. Then take a look at your financial goals. If you don't have any goals, now would be a good time to consider some. Here are a couple of questions and suggestions for you. Do you have any savings for an emergency? If not, that should be a primary consideration. A possible $500 to $2,000 in a savings account will take a lot of ...

No shortage of mistakes in money matters

By Leanne | | Tip of the Week

Someone asked me the other day what makes me qualified to give advice on money matters. I replied that I have seen a lot of people make some simple money mistakes. In most cases, poor decisions are because of personal stress and not understanding the consequences of our actions. Here are some of the most common mistakes I have seen people make when it comes to dealing with their financial situations: > Not talking to your spouse and family. When situations change or financial decisions have to be made, talk to everyone that is going to be affected by your decision. Buying a new car, losing or quitting a job, reductions in household income affect everyone. Get everyone involved so you are all on the same page. > Living off credit. Many people think they are doing OK without a budget, but use their credit cards for gas, clothes, and ...